The Russia-Ukraine war won’t derail the recovery

The US economy's performance in the past few months has been better than most people expected—or even realized. While Omicron took infection rates to a new high, little trace appeared in economic data. Inflation and related problems, such as tangled supply chains, may continue to challenge business leaders and policymakers, but the US economy is performing well by most measures:

The unemployment rate is already back to the full employment level.

The labor force participation rate has started to pick up, as some of the folks who left the labor force are coming back to work.

Corporate profits are more than satisfactory. Profits in Q3 2021 were 21% above the prepandemic level. That’s much better than many businesses had reason to expect when the pandemic first hit in March 2020.

Strong profits have supported business investment. The pandemic shifted investment away from buildings and toward equipment and information products. 1 But the willingness to invest suggests that businesses are surprisingly optimistic about the future.

The pandemic drove the adoption of technology and—as a consequence—appears to have accelerated labor productivity growth. Previous Deloitte forecasts assumed trend productivity was less than 1%. But productivity growth has remained surprisingly strong during the recovery from the pandemic, about 2% over the four quarters to December 2021. If productivity growth remains high, many of the long-term issues facing the US economy—such as financing social security—will likely become considerably easier to solve.

But just as Omicron’s potential to impact the economy waned, geopolitical tensions increased. The Russian invasion of Ukraine is not likely to derail the US recovery, but it will push up inflation in the short run.

The US economy is likely to feel the impact of a continuing Ukraine crisis through two main channels.

Most importantly, the price of oil is likely to remain higher than it would have otherwise—although how much higher is an open question. Russia produces about 12% of global crude oil supplies. Sanctions may remove some of this oil supply, as the United States (and possibly some European countries) reduce or end purchases of Russian oil.

However, oil is a global, fungible commodity and Russia can still sell oil to non-boycotting nations. That would release other oil for shipment to boycotting countries without affecting the global price of oil. Of course, payments may be more difficult, and Russia may need to sell its oil at a discount. But the size of the supply shock may be more limited than that 12% figure suggests.

Europe's heavy dependence on Russian natural gas suggests that the EU's economy will experience slower growth—or, in the extreme case, a recession. The EU is a major trading partner of the United States, accounting for more than 15% of US exports. On top of a direct decline in demand, dollar appreciation reflecting the relative safety of the United States will make US goods less competitive. Both would reduce the contribution of exports to US GDP growth.

The combined impact is not large enough to generate a recession in the United States. But growth could slow down. And inflation would pick up, at least in the short term. Our baseline forecast assumes a US$15 per barrel rise in the price of oil , which leads to an extra half a percentage point rise in the consumer price index (CPI) in 2022 (with most of the rise occurring in the second quarter). That's not huge, but during a period when the Fed is struggling to control inflation , it presents policymakers with a big problem.

Before the invasion, we had penciled in five 25-basis-point Fed hikes in 2022, starting in March. Despite this bump in inflation, we don't think the Fed's interest rate trajectory is likely to change. Our reasoning: The Fed knows that the extra inflation is (to use that banished word) “transitory.” And the extra inflation will be associated with some additional unemployment, which would call for the Fed to ease. In our forecast, the reasons for easing offset the reasons for raising rates, leaving policy unchanged from the preinvasion path.

We've also assumed a small impact on exports. First, growth in Europe is likely to take a hit of as much as half a percentage point, even if natural gas deliveries from Russia aren't interrupted. Second, any geopolitical crisis pushes investors to buy safe assets, mainly US dollars. The dollar's appreciation will make US exports less competitive.

And keep in mind: COVID-19 hasn't gone away. While the probability of the disease becoming both less deadly and endemic is rising, new mutations could change things quickly. We continue to carry a scenario in which COVID-19 once again slows the economy.

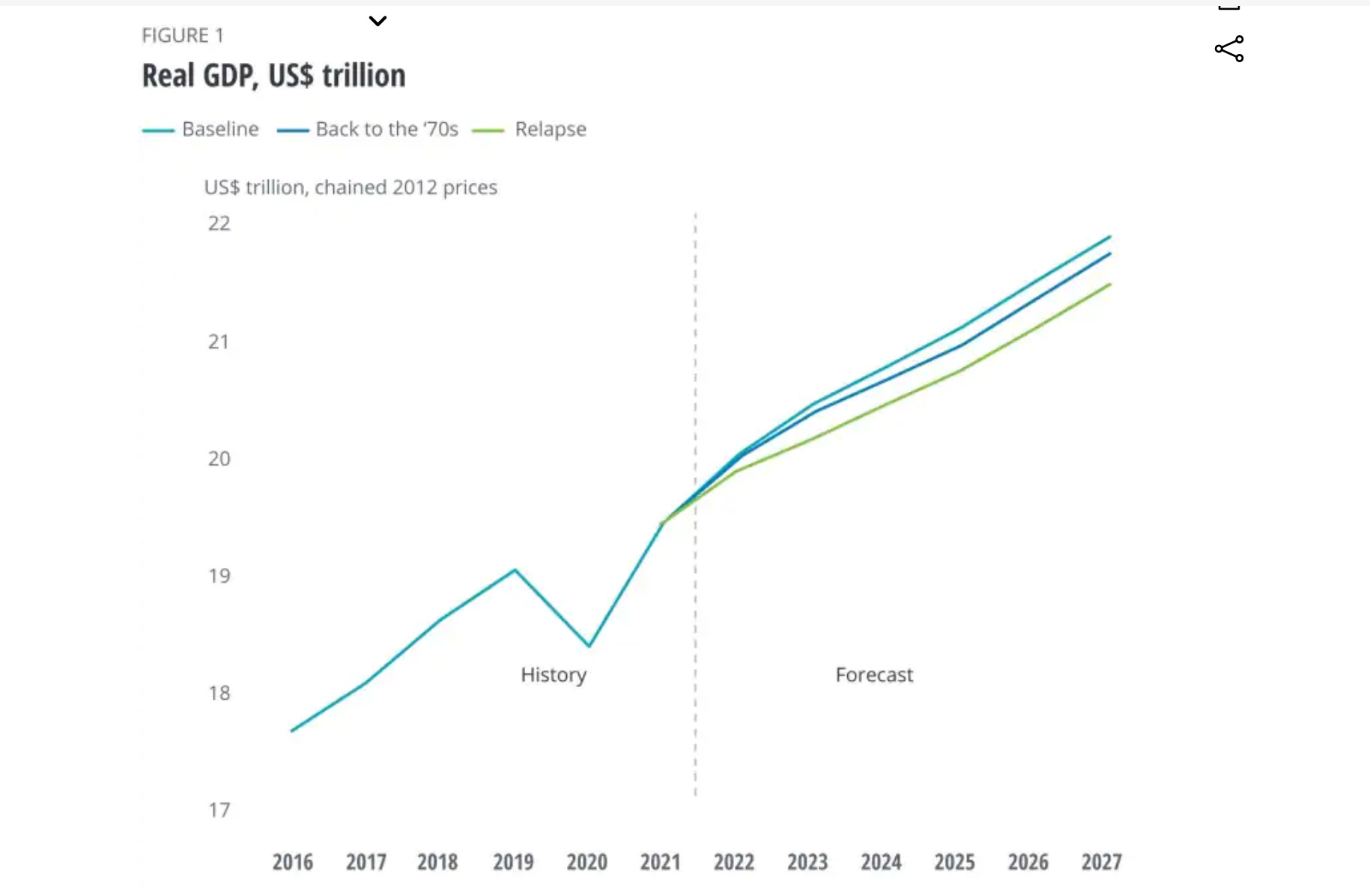

Scenarios

Baseline (55%): Growth continues in 2022 as the impact of COVID-19 wanes, although some slowing occurs as the economy reaches full employment, monetary policy becomes tighter, COVID-19–era fiscal impulse reverses, and the Ukraine crisis raises energy prices and the dollar temporarily. Households continue to increase spending on pent-up demand for services such as entertainment and travel. However, spending on durable goods stalls as consumers switch back to prepandemic patterns. Business investment continues to grow rapidly, particularly in information processing equipment and software. Investment in nonresidential structures remains weak, however, as the oversupply of office buildings and retail space weighs on the market. The infrastructure spending bill raises the level of government spending modestly for most of the forecast period. All of this helps elevate demand above the pre–COVID-19 trend for several years. Inflation remains above the Fed’s target in 2022, but gradually settles back to the 2% range as demand for goods falters and businesses solve their supply chain issues. The pandemic jump-starts the widespread adoption of new technology, leading to faster productivity growth. The unemployment rate gradually falls back to below 4%. The Fed raises rates at a relatively fast pace in 2022 out of concern about inflation, then slows rate hikes as inflation falls back to the normal range.

Relapse (15%): The discovery of the Omicron variant underlines the risks that COVID-19 continues to pose to the US economy. New variants are constantly being found.2 In this scenario, the current vaccines are not as effective against one or more new variants. People return to social distancing and cut back on purchasing services that are perceived as “risky.” This slows growth substantially. A muted government response results in financially stretched businesses failing and weakened balance sheets create the conditions for a more traditional, slower recovery from the recession. After continued outbreaks, consumers permanently reduce spending on travel, entertainment, food, and accommodations, requiring a painful readjustment of the economy.

Back to the ‘70s (30%): Households and businesses see price hikes from pandemic-related shortages and react by raising prices and wages. The reaction, and consequent rise in inflationary expectations, creates an inflationary spiral. Consumer prices are rising at a steady rate of over 5% by the end of 2022, causing the Fed to raise interest rates to limit demand. In 2023, inflation continues, but a “growth recession” causes the unemployment rate to rise. The Fed is reluctant to engineer an actual recession, and inflation settles in at a 4% rate over the five-year forecast horizon.

Consumer spending

The near-term outlook for consumer spending turns on two big questions:

- Will consumers spend down all those pandemic-era savings? In 2020, during the height of the pandemic, households saved about US$1.6 trillion more than we forecasted before the pandemic. Some of that went into investments, but many households have a lot more cash on hand now than they normally would want. How much of that will they spend as the pandemic impact wanes? One possibility is that many consumers will remain cautious and hold on to those savings even as they are able to go out and spend. Another possibility: Spending booms for a while longer as the impact of COVID-19 continues to wane. The baseline Deloitte forecast assumes a modest decline in the savings rate below its long-term level, and that’s enough to support continued growth in consumer spending. But spending could be even stronger this year if households decide to cash in more of those savings.

- When consumer services recover, what happens to durable goods? The pandemic sparked a remarkable change in consumer spending patterns. Spending on durable consumer goods jumped US$103 billion in 2020, while spending on services fell US$556 billion during the same period. Households substituted bicycles, gym equipment, and electronics for restaurants, entertainment, and travel. Once households can again purchase services, will they begin buying fewer goods? That may be happening, as by December 2021, durables spending was down 14% from the peak in March 2021.

Housing

The housing sector has outperformed the broader economy in the wake of the pandemic, as buyers and sellers found ways to navigate the pandemic’s restrictions. A host of factors combined to boost housing demand over the past year:

- Continued strong economic position of high-wage remote workers

- Growing expectations that remote work will persist after the pandemic

- Historically low mortgage rates

- Millennials moving into prime home-buying

Business investment

Businesses have ramped up investment since the initial impact of the pandemic, but they have been selective about what they are investing in.

Foreign trade

The Ukraine crisis is likely to make things more difficult for US exporters. Lower demand from Europe (market for 15% of US exports) and a higher dollar will create some short-term challenges.

Government policy

President Biden’s Build Back Better plan appears unlikely to pass at this point. But if it does pass, it will likely be considerably smaller than originally planned. That leaves federal budget policy on a much more modest path than what might have been expected six months ago.

Labor markets

The conversation about labor markets has switched—and fast. Not long ago, employment was about 10 million below the prepandemic level and the main question was how difficult it would be to get all those workers back on the job. Now business commentary is full of talk about labor shortages and stories about employers struggling to find workers. That seems a bit odd since employment is still lower than the prepandemic level.

Financial markets

The Fed’s actions have been one of the bright spots of the US response to the pandemic. When the virus first began spreading, there was a significant possibility that a financial market meltdown would exacerbate the country’s economic problems. The Fed’s prompt and strong actions kept financial markets liquid and operating, preventing that additional level of pain.

Prices

The news media has been flooded with reports about inflation for some time. Before the Ukraine crisis, that commentary tended to underplay how much of the rise in prices was due to specific supply chain problems that were likely to be alleviated over time. Businesses were already finding ways around some of these shortages, and the rotation of consumer spending from goods to services is also removing some pressure on supply chains. The possibility of a significant bump in prices in Q2 from higher oil prices complicates, but does not negate, that picture. There are some other likely impacts on prices (such as a rise in food prices as Ukrainian and Russian wheat exports disappear this year). These may add to short-term price pressures. The real question, however, remains the same as before the Ukraine crisis: whether inflation becomes baked into the economy. We have increased the probability of our “Back to the ‘70s” scenario for this reason.

沒有留言:

張貼留言